Crisis alpha with a higher return potential

Recent market volatility is a powerful reminder of the value of including trend–following strategies in a portfolio due to their strong defensive properties.

Highlights

- Trend-following strategies, backed by their long and proven track record of defensive performance, have played a critical role in portfolio crisis risk offset.

- Our research found that risk-taking in a trend-following approach is dominated by beta timing, rather than relative value investments implied by trend positioning within asset classes.

- Furthermore, beta timing is the main driver of “crisis alpha” of trend following, exhibiting a negative correlation to equities, particularly during periods of market stress. In contrast, relative revalue contributes very little to crisis alpha.

- This suggests it may be possible to keep the crisis alpha characteristics intact while reallocating the relative value component toward a richer set of alpha signals.

- Increasing exposure to trend beta and complementing it with a market neutral strategy, such as carry, results in a more resilient portfolio with a similar crisis alpha profile but higher return potential, particularly in environments where equities are performing well.

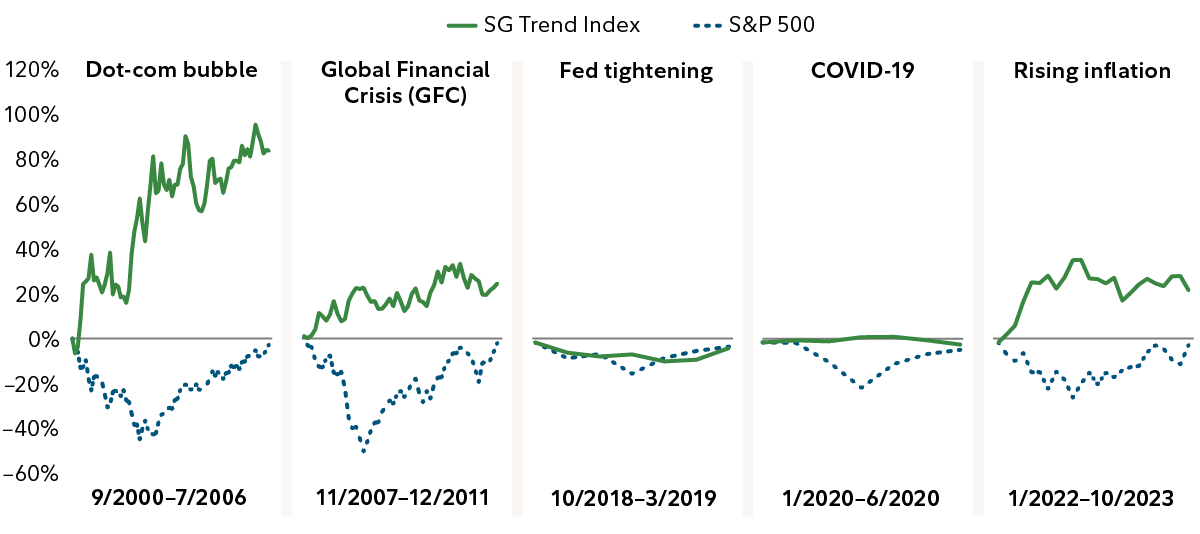

Source: Fidelity Investments, Bloomberg Finance LP, as of 12/31/25. Past performance is no guarantee of future results. Blue line represents S&P 500 drawdowns. Green line represents the SG Trend Index during those equity drawdowns, with performance reset after each drawdown. See endnotes for index definitions.